Reviewing Our 2013 Picks: MPEL, MSG, TTWO, YHOO, FL

5th Street Research’s Buy Recommendations Easily Outperform The Market

Having been away from the market with other obligations for the past month or so, I thought it would be interesting to review our 2013 picks before making any new recommendations in 2014. Since launching in late September, we have published buy recommendations on 5 different companies: Melco Crown Entertainment (MPEL), Madison Square Garden (MSG), Take Two Interactive (TTWO), Yahoo (YHOO), and Foot Locker (FL). While the S&P 500 and Nasdaq finished out the year strong, our picks have easily outperformed the broad markets, returning an average of 16.5% vs. 7.5% for the S&P 500. A brief update on each of our recommendations below…

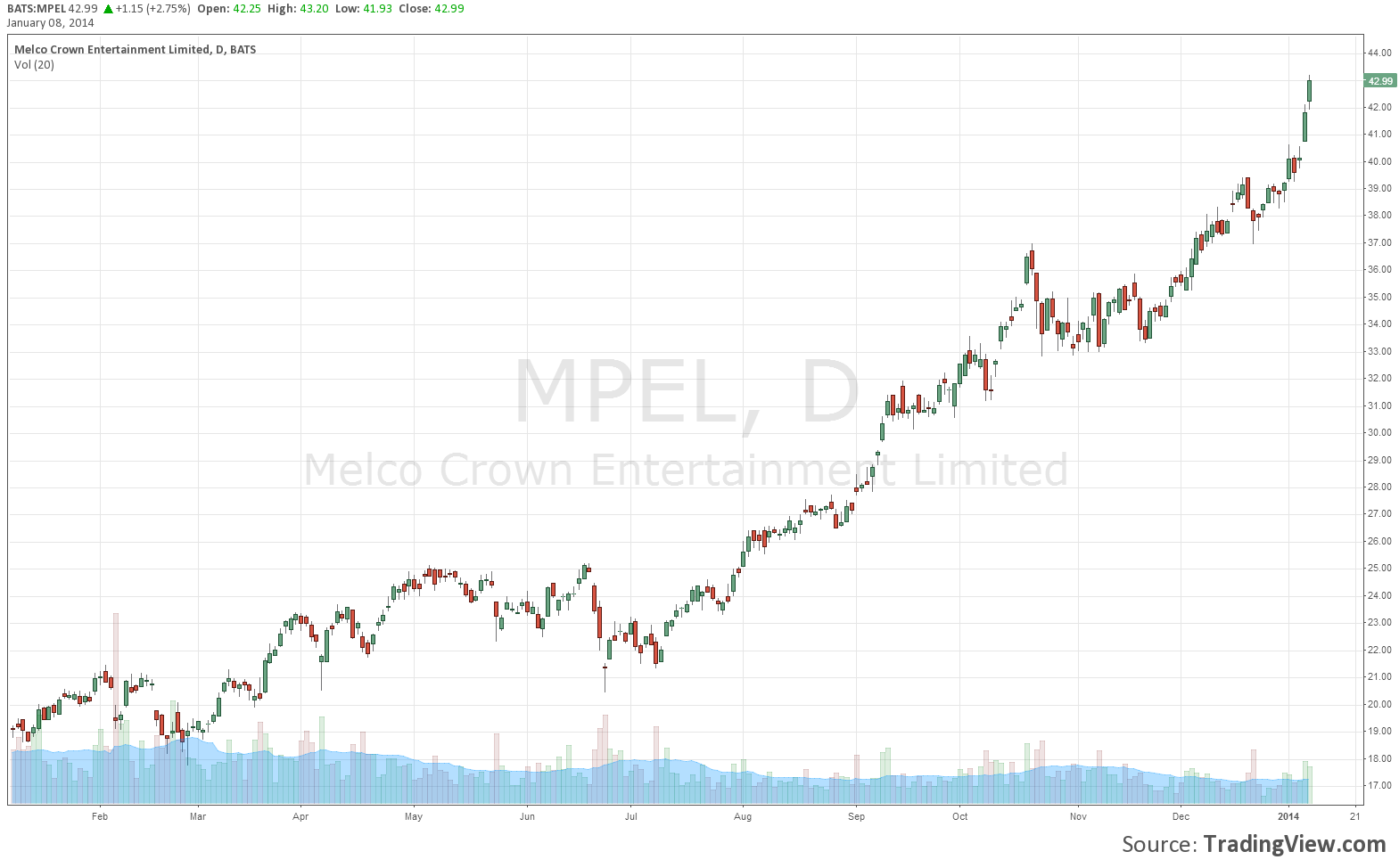

Melco Crown Entertainment (MPEL): City of Dreams Manila and Studio City Macau

Buy Recommendation

Published 9/27/2013: The Best Bet in Macau is Melco Crown Entertainment (MPEL)

Price Then: $31.60

Price Now: $42.99

% Change: +36%

Macau as a whole has been the recipient of quite a bit of attention around here since launching, and for good reason… Macau has been the world’s fastest growing economy over the past decade with average annual GDP growth near 15%. It generates more than 7x the revenue of Las Vegas and is the gambling epicenter of the world. Melco Crown’s City of Dreams is one of the most impressive properties in Macau and dominates the ultra important “Premium-Mass” market in the region. MPEL’s revenues and profits stand to explode over the next two years as they open two new massive properties, Studio City Macau and City of Dreams Manila. Studio City boasts the best location on the Cotai Strip, Macau’s version of Las Vegas Blvd., and is poised to be one of the biggest beneficiaries of the continued growth of the Macau. Despite the 36% gain since our initial recommendation of their shares, I continue to view MPEL as a strong buy for the foreseeable future.

Madison Square Garden (MSG): Hidden Assets and Rising Sports Franchise Valuations

Buy Recommendation

Published 10/11/2013: Significant Value in Madison Square Garden (MSG)

Price Then: $57.54

Price Now: $56.72

% Change: -1.4%

Madison Square Garden has been the laggard of our model portfolio thus far, currently down 1% since our original recommendation. The New York Knicks have gotten their season off to a terrible start this year, however there has been little to no other news or events out of MSG in the past 3 months. With the Madison Square Garden renovation project finally complete, cash flows and earnings will start becoming normalized for the first time since their IPO. The real story here though remains the hidden value of the company’s array of assets. As the owner of the Knicks and Rangers, MSG Networks, Madison Square Garden Arena and its associated air rights, and numerous other venues/ assets; MSG remains greatly undervalued when using a sum of the parts analysis. This one may require some patience, but I continue to view MSG as a strong buy.

Take Two Interactive (TTWO): Massive Cash Hoard, Best IP Portfolio in the Industry

Buy Recommendation

Published 10/15/13: GTA V Makes Take Two Interactive (TTWO) a Steal

Price Then: $16.94

Price Now: $17.80

% Change: +5%

Although shares of Take Two have appreciated since our recommendation, they have lagged the market, which is somewhat perplexing after Grand Theft Auto V shattered analyst estimates and became the highest grossing entertainment release ever. While analysts anticipated TTWO would sell 18 million units of GTA V during their most recent quarter (a number I reported would prove to be very low), 25 million copies were actually sold. TTWO stock failed to jump on this news though, they actually traded down sharply the next few sessions as management failed to give much clarity regarding their future pipeline/ next blockbuster release. TTWO’s haul from GTA V should leave the company with more than $1B worth of cash on their balance sheet. With a market cap of only $1.6B, this cash hoard is substantial. Take Two also owns arguably the most valuable intellectual property portfolio in the industry with proven franchises such as GTA, BioShock, Red Dead Revolver, Max Payne, and NBA 2k. Despite management remaining mum on the next big release for now, they have an amazing track record when it comes to making hits. Everything considered, I see fair value for Take Two stock between $22-$24, at least 25% upside from today’s closing price. I maintain a buy rating on shares of TTWO.

Yahoo (YHOO): Alibaba Stake Continues to Create Value, Meyer on Acquisition Spree

Buy Recommendation

Published 10/15/2013: Amended Alibaba Agreement Makes Yahoo (YHOO) More Attractive

Price Then: $33.38

Price Now: $41.03

% Change: +22.9%

As Alibaba continues their rapid growth, Yahoo continues to reap the rewards. Despite a core business that is still struggling to gain momentum, Yahoo had a great 2013 with shares more than doubling during the year. New CEO Marissa Mayer has been on quite the shopping spree since taking the helm, with Yahoo acquiring 28 companies in 2013, including a $1B purchase of Tumblr. Mayer has made it clear that she intends to ensure Yahoo remains the world’s homepage while also placing a large emphasis on mobile and content creation. In a demonstration of their commitment to content, Yahoo recently hired Katie Couric as a ‘global anchor’ and released a new News Digest App. It is yet to be seen how any of this efforts will pan out, but if nothing else, Mayer has been ambitious. YHOO should still see some upside from Alibaba as it nears its inevitable IPO and could get a lift from the news when announced, but shares aren’t as much of a bargain as they were 3 months ago. If you already own YHOO stock I wouldn’t be in any rush to sell it, but I wouldn’t be in any rush to go out and buy more either. I view shares as undervalued still with 10-15% upside, but would need to see core operations start to show signs of improvement before considering YHOO a strong buy at current levels.

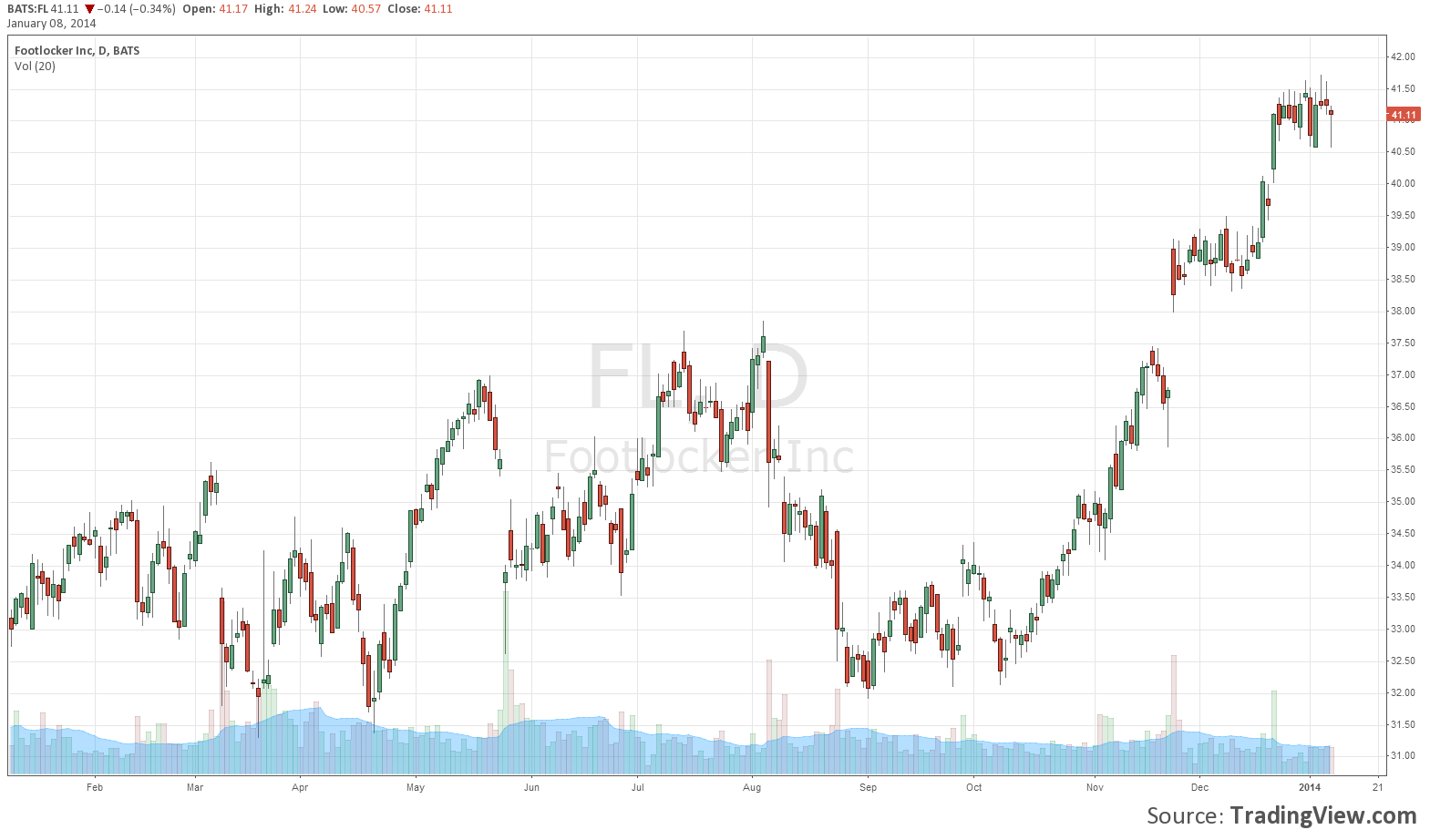

Foot Locker (FL): Buy into Nike, Adidas, and Under Armour’s Growth at a Discount

Buy Recommendation

Published 10/26/2013: Try Foot Locker (FL) on for Size

Price Then: $34.20

Price Now: $41.11

% Change: +20.2%

Last but certainly not least of our recommendations during 2013 was Foot Locker. The athletic apparel industry has been one of the strongest performers of the past 25 years. Nike is one of the all time great growth stocks and shows no sign of slowing momentum. Adidas and Under Armour fit the same mold. Justifiably so, all three of these companies trade at lofty valuations. Foot Locker is the largest retailer of athletic shoes in the US, dominating the market with the portfolio of brands including FootAction, Eastbay, Champs, and of course their namesake stores. Management has proven to be shareholder friendly, approving a $600 million buyback and an 11% dividend hike last year. While many retailers reported lackluster earnings in their most recent quarter, Foot Locker easily exceeded both earnings and revenue estimates. Despite all of this, shares still trade at a significant discount to retailers such as Finish Line and Dick’s Sporting Goods. The athletic apparel industry has shown no signs of slowing, and Foot Locker is as well positioned to benefit from this trend as anyone. As long as they continue to trade at such cheap valuations relative to their peers, I will continue to maintain a buy rating on shares of FL.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article.